ByPeter Norman

Total Canada-wide housing starts rose to 147,500 units seasonally adjusted at annual rates (SAAR) in the third quarter of 2009, according to the Canada Mortgage and Housing Corporation. That’s up about 15 per cent from the second quarter. The upturn in starts in the most recent quarter represents an encouraging sign for those anxious to see the depths of last year’s sudden recession behind us.

Also encouraging is that the rise in the third quarter was broadly based, with gains registering in all regions ranging from a six per cent rise in Ontario to a 29 per cent increase in B.C. Both apartment and single-family housing starts were up in that quarter.

Obviously, a certain amount of context is required to understand that, although the third quarter movement was up, it was still a fairly poor quarter. Beyond the past few recessionary quarters, the last time the Canadian home building industry turned in a quarter below 150,000 units SAAR was nine years ago, and this pace of activity is some 35 per cent below the average annual rate over the five years leading up to 2008.

Signs of life in new construction are coming on the heels of stronger activity in the existing home sales market. According to the Canadian Real Estate Association, the number of homes sold through the Multiple Listing Service has been rising steadily from a low in January. The buoyancy in resale markets has been a truly remarkable story. In the six months prior to August, despite being at the tail end of a long recession, the number of home sales actually rose over the same period in 2008. On a seasonally adjusted basis, average prices in August reached well above their pre-recession levels.

Pent-up Demand and Affordability Driving Market

Canada’s economy is now very likely in a recovery, with gross domestic product estimated to be turning positive in the third quarter, following three quarters of steep declines. The jobs market, which has already shed some 415,000 jobs from peak to trough in this recession, is still lacklustre, and promises slow growth at best over the next year or so.

It is highly unlikely we’ll have buoyant housing markets in this country concurrent with weak labour markets, so any optimism over the strength and longevity over this housing recovery should be tempered.

Clearly pent-up demand from the recession and strong affordability — in particular the exceptionally low interest rates — are driving current trends. Home buyers now enjoy posted five-year mortgage rates below 5.5 per cent (and effective rates after discounting close to four per cent). Rates this low are virtually unprecedented, and are certainly likely to rise, perhaps quickly, starting early next year.

It is encouraging to see such positive numbers coming out of the new housing and resale markets. Builders and others with an interest in the industry should remain cautious however, as higher interest rates and the depletion of pent-up demand may lead to a generally longer and slower recovery period ahead.

Spin-off Effects Hitting Suppliers

One of the clear victims of the recent recession has been residential investment (new construction and renovations combined), which has declined some $8.4 billion between the first halves of 2008 and 2009.

The effects are being felt throughout the supply chains, from building materials and distribution through to related services. Eventually, we’ll get a fuller picture of the negative effects on Canada’s building products sector from this recession. For now, it is necessary to turn to our economic impact model in order to gauge the likely impact recent declines in investment may be having.

Because of the large spin-off effects from housing construction, the annualized decline in residential construction investment has contributed to the decline in total output across Canada’s economy to the tune of an estimated $15.1 billion, along with the loss of considerable jobs.

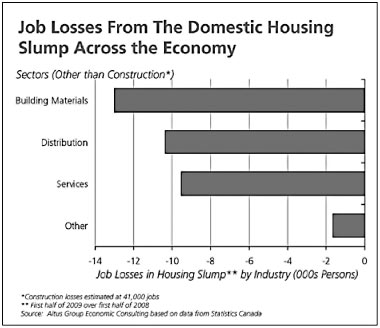

Through the recession, jobs directly related to residential construction declined by an estimated 41,000 persons in Canada, while related jobs in manufacturing, distribution, services and other sectors fell by an additional 35,000 persons. Among these spin-off jobs, the building materials manufacturing sector has lost of almost 13,000 jobs, in addition to 10,400 jobs related to the distribution of building products (the wholesale, retail and transportation sectors) and 9,500 job in various companies providing services to the residential construction sector.

Among the building materials sector, the most significant pain has been felt in wood materials manufacturing (loss of 5,000 persons), steel products (2,200 persons) and the concrete and plastics sectors (1,200 persons each).

The worst of the housing slump is likely behind us, but it may be a long slow recovery for the building materials sector.

Peter Norman is member of the CHBA Economic Research Committee and is Senior Director of Economic Consulting at Altus Group (formerly Clayton Research), a firm of urban and real estate economists.