ECONOMICS

Don’t Stress the Stress Tests:

Housing Starts to Remain Stable in “Lukewarm” Market

By Peter Norman

As we move through the first quarter of 2018, conditions in the housing market are largely evolving as previously expected. Headwinds caused by the expansion of the mortgage stress tests at the beginning of the year alongside modestly higher interest rates and perhaps a general sense of economic uncertainty are manifesting into more turbulence, especially in resale markets, but a number of important mitigating factors continue to support housing demand to ensure that new housing starts remain largely buoyant and steady.

Total Canada-wide housing starts rose to about 233,400 units seasonally adjusted at annual rate (SAAR) in the 4th quarter of 2017, according to the Canada Mortgage and Housing Corporation (CMHC), up 4% from the 3rd quarter. But 2018 is off to a slower, albeit still reasonable, start. In the first two months of the year, average housing starts were 222,500 units SAAR down about 5% from the fourth quarter. Both apartment and single-family starts shared in the decline at the beginning of 2018, but in general terms, the level of starts for apartment units continues to be relatively buoyant whereas single-family appears weak.

Geographically, the decline was broadly based with most provinces participating in the moderation; exceptions were Ontario (up 30%), Nova Scotia (15%) and Saskatchewan (4%).

Total full-year housing starts ended up at 219,760 units, endowing 2017 with the highest total housing starts in the past 11 years (since before the recession). After a surprisingly strong 2017, Canada-wide total housing starts are expected to fall back in 2018, with all regions except Alberta (which is still recovering from its recent recession) contributing to the moderation.

In 2019, total housing starts are forecast to remain pretty steady, as some improvement in single-family starts is offset by a modest decline in apartments. Quebec, Ontario and B.C. will each moderate in 2019 coming off of recent highs counterbalanced by improvements elsewhere.

The Temperature of Things to Come

The weakness so far in 2018 and the relative steady nature of the forecast is related to the “hot” and “cold” factors affecting housing demand that should combine for a “lukewarm” market.

“Hot” includes the very strong economic momentum at the end of 2017, which is setting up for some significant tailwinds for housing demand and housing starts. Job growth accelerated through the year and stood at 374,000 net new jobs on a year-over-year basis in Q4. Historically, a surge in job creation is positive for housing demand and higher housing starts, but typically with a lag.

The lag may be longer this time around due to the “cold” conditions including emerging headwinds in form of the B-20 mortgage stress tests, modestly rising interest rates, continued price and supply constraints in major cities, uncertainty surrounding NAFTA negotiations and threatened specialized U.S. tariffs on selected products.

On net, housing markets are going to look turbulent through the first half of 2018, but expect stronger housing starts in the second half. Home buying intentions remain elevated at the Canada-wide level, and we expect that motivated buyers will drive activity later in the year once the market settles.

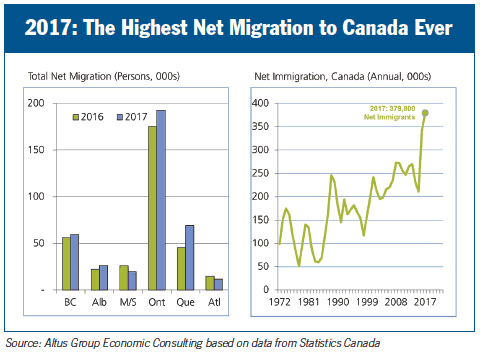

A key demand driver in the current forecast is migration. Net migration is a significant driver of housing demand (both ownership and rental) and total net migration to Canada continues to be on the rise. 2016 saw some 340,000 net new migrants come to Canada, fully 61% higher than 2015. And in 2017 the number rose a further 12% to a record of almost 380,000 net new persons. Thanks to this rise nationally, the regional pattern (which is also inclusive of net migration between provinces) shows recent gains in Quebec and Ontario with most other regions remaining about on par with a year prior (see chart).

Historically, international migration has an impact on rental markets right away as about 80% of new immigrants establish rental households upon landing. But ownership rates tend to converge with the general population over a period of about nine years. Migration has been on the upswing for several years now, but the remarkable jumps in the past two years described above are fostering stronger rental demand today and will translate into improved home sales over the next few years.

Peter Norman is VP & Chief Economist at Altus Group, and leads a national team of economic advisors providing policy analysis, feasibility assessment, and economic intelligence to the home building and real estate industry. He can be reached at peter.norman@altusgroup.com.

External Links: Associations & Governments. Builders & Renovators . Manufacturers & Suppliers

Home . About Us . Subscribe . Advertise . Editorial Outline . Contact Us . Current Issue . Back Issues . Jon Eakes

© Copyright - Work-4 Projects Ltd.